Originally posted in The Financial Express on 2 April 2023

Whether the fiscal framework of the fiscal year 2022-23 (FY23) was designed considering the correct set of assumptions remains a critically important question. While the economy was already reeling under immense pressure due to the ramifications of the Covid-19 pandemic, the situation on the eve of presentation of FY23 budget was exacerbated by the rising pent up demand and price hike in global commodity market consequent to the advent of Russia-Ukraine war in late February 2022. Regrettably, FY23 budget failed to take cognisance of the emerging scenario and the new realities that should have informed budget design and fiscal-public expenditure proposals. This resulted in a fiscal framework that was rather formulaic in nature and driven by business-as-usual considerations, i.e., lofty targets were set that had a high probability of missing their marks by a considerable margin at the end of the fiscal year. As the halfway marks become available, it is safe to anticipate that the probable will become the reality as the current fiscal year reaches the finishing line. Drawing lessons from this experience, the design and fiscal targets of the upcoming FY24 should be set in a realistic manner, taking cognisance of the current macroeconomic trends – both domestic and external.

The issue of realistic target setting could take the case of revenue mobilisation as a key reference point. For instance, while proposing the budget for FY23, the targeted growth of revenue earnings was set at 11.3 per cent over the revised budgetary target of FY22. However, if the realised revenue mobilisation of FY22 is considered, the growth target for FY23 actually turns out to be almost threefold, at 31.8 per cent. As it so happens, according to the Ministry of Finance (MoF) data, revenue mobilisation decreased by (-) 3.1 per cent during the first six months (July-December) of FY23. This implies that if the annual growth target of 31.8 per cent is to be achieved, then revenue earnings will need to increase by an unrealistic 67.4 per cent over the remainder (second half) of FY23. Revenue mobilised by the National Board of Revenue (NBR), which accounts for about 85 per cent of the total targeted resource envelope, decreased by (-) 4.0 per cent during the July-December period of FY23. [Curiously, data provided by the NBR itself posted 11.0 per cent growth during the July-December period of FY23. It may be noted that the July-December FY2023 tax collection figure reported by the NBR surpasses the MoF figure by about Tk 44.0 billion. Also, the two agencies reported widely different figures as regards the tax collected by the NBR during July-December FY22. Indeed, it is this figure of FY22 which is the primary reason for the divergence. MoF reported that Tk 1468.59 billion was collected by NBR during the July-December FY2022 period whereas the figure reported by NBR for the same period is Tk 1310.35 billion. As a result, the growth figure reported by NBR appears to be much higher than the MoF figure.]

The decline in NBR tax collection can be primarily attributed to the fall in VAT and import duty collection. This, perhaps, is a reflection of the various import-related restrictions imposed by the government in view of the ongoing foreign currency crisis. On the other hand, this is also indicative of a possible slowdown in economic activities. If this indeed be the case, then any significant increase in revenue mobilisation over the short term is highly unlikely.

If the current trend of revenue mobilisation persists, a large shortfall (i.e., the gap between the revenue mobilisation target and actual attainment) at the end of FY2023 will become inevitable. In December 2022, Centre for Policy Dialogue (CPD) came up with the projection that the total revenue shortfall in FY23 is likely to be Tk 640.0 billion. Taking advantage of the latest available data from both MoF and NBR, and considering the trends of other macroeconomic correlates, we now project that the revenue shortfall at the end of FY23 could reach approximately Tk 750.0 billion, with total revenue collection being about Tk 3580.0 billion. In this connection, it must be noted that the International Monetary Fund (IMF) has projected the total revenue mobilisation of FY23 and FY24 to be nearly Tk 3876.0 billion and Tk 4549.0 billion, respectively. If the aforementioned CPD projection holds and the IMF projection for FY24 is to be achieved, then total revenue mobilisation in FY24 will need to grow by about 27 per cent – a daunting task indeed. Furthermore, as a quantitative performance criterion to avail of the IMF loan facility, the floor of tax revenue collection at the end of FY23 has been set at Tk 3456.30 billion. This clearly illustrates that the government has an uphill battle in the area of revenue mobilisation for both current and upcoming fiscal years if it wants to avail of the future instalments of the IMF loan.

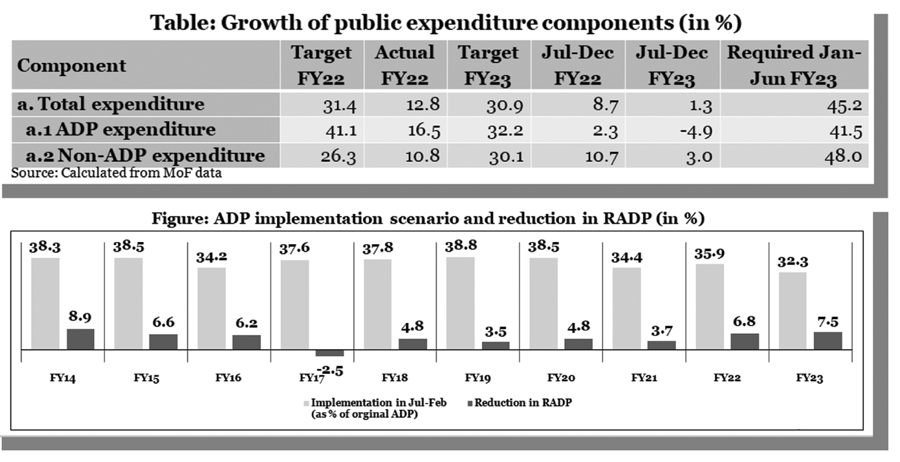

The failure to utilise planned budgetary allocations has been a regular feature in Bangladesh’s fiscal framework. Regrettably, this trend has continued in FY2023. According to the MoF data, total public expenditure recorded a paltry growth of 1.3 per cent during the July-December period of FY2023 (Table 3.1). The most alarming fact in this regard is that the annual development programme (ADP) expenditure recorded a negative (-) 4.9 per cent growth during the aforementioned period. [The discrepancy in data reporting is observed once again in this case. According to the data from Implementation Monitoring and Evaluation Division (IMED) of Ministry of Planning, ADP expenditure increased by 7.3 per cent during July-December of FY2023.] Whether it is due to limited resource availability owing to the fall in revenue mobilisation, the inability to implement the large number of projects, or is a result of the austerity measures taken by the government remains a critical question in this backdrop. ADP and non-ADP expenditures will need to increase by 41.5 per cent and 48.0 per cent, respectively, over the remainder of FY23, to reach the programmatic public expenditure targets.

The data available from the IMED gives a more updated picture as regards the ADP implementation scenario. During the first eight months of FY23 (July-February), actual expenditure on account of ADP implementation was 32.3 per cent of the originally planned allocation of Tk 2460.66 billion which is the lowest in the last decade. The utilisation of project aid (35.7 per cent) was marginally higher than the corresponding period of FY22 and was in line with the trend of last three-four years. It was the Power Division that primarily drove the utilisation of project aid (PA). The utilisation of the local resource (taka) component (30.2 per cent) was the lowest since FY14. Of the top ten ministries/divisions with a combined share of 72.5 per cent of the total ADP allocation for FY23, four were not able to utilise their respective allocations at the average level. These are the Ministry of Science and Technology, Ministry of Primary and Mass Education, Health Services Division and Secondary and Higher Education Division. In this connection, it must be mentioned that in the budget speech for FY23, ensuring timely completion of projects in education and health sectors was identified to be one of the major challenges for FY23.

In view of the slow pace of implementation, a number of major government sectors (e.g., Education, Transportation and Communication, Health, and Power and Energy) were subjected to significant reduction in the revised ADP (RADP) for FY23. The ADP for FY23 was slashed by Tk 185.0 billion (or 7.5 per cent) which brought the size down to Tk 2275.66 billion. The reduction was fully on account of the PA component with the taka component remaining unchanged. This appears to be rather counterintuitive for two reasons: first, the rate of implementation of the PA component was better than that of the taka component, and second, in view of the ongoing foreign currency crisis, ‘utilising funds available through foreign assistance’, should have been given highest priority as mentioned in the budget speech.

Given the shortfall in revenue collection, inability to spend budgetary allocations could give policymakers some ‘relief’. As a consequence, the level of budget deficit may not become a major concern in FY23. However, this trade-off, as CPD has repeatedly pointed out, is a false relief brought with significant macroeconomic costs. Along with this, the composition of deficit financing should trigger some reasons for concern. Comparing the July-December period of FY23 to the corresponding period of FY22, the government’s reliance on borrowing from the banking system has seen some rise. At the same time, due to lower net sales of national savings certificates, net non-bank borrowing has increased rather slowly. Given the persistent inflationary pressure in the economy, the government may need to continue to proactively borrow from non-banking sources in the coming days. However, as mentioned in the previous section, whether it will be possible remains a concern.

In light of the preceding discussion, the following suggestions are placed before the policymakers to take into account while formulating the national budget for FY24:

• The personal income tax (PIT) structure in the FY2023 budget has remained mostly unchanged from the one introduced in FY2021. CPD has argued that lowering of the highest tax rate (from 30 per cent to 25 per cent) went against the idea of tax equity. In the FY24 budget, the maximum tax rate should be restored to 30 per cent for highest cohort of earners.

• Given the increased pressure of the commodity price hike, particularly those of food items, the tax-free income threshold for personal income should be increased to Tk. 3.50 lakh. As an alternative, in order to give the low-income earners some respite, the second PIT slab, which is 5 per cent for an additional Tk 1 lakh, should be raised to Tk 3 lakh.

• In the FY23 budget, the rate of investment tax rebate was fixed at 15 per cent on the eligible amount. This means that higher taxpayers, i.e., top earners receive higher tax rebate benefits, whereas those with annual income below Tk. 15 lakh are not eligible to get any additional tax benefits. The withdrawal of this provision needs to be considered in the FY24 budget.

• The FY23 budget also increased the allowable ceiling of perquisite from Tk 5.5 lakh to Tk 10 lakh. Accordingly, individuals with annual income ranging between Tk 16.5 lakh and Tk 30 lakh will receive additional tax benefits of up to Tk 112,500 per year. This is another instance where the tax policies favour high-income groups. The FY24 budget may consider eliminating this clause.

• All ad-hoc provisions of tax incentives should be stopped from FY24. NBR needs to be selective and careful in the next fiscal year as more demand for incentives will be lined up in view of current economic situation. Proper cost-benefit analysis must be conducted before coming up with new provisions. ‘Sunset clauses’ should be introduced in case of existing provisions. There should also be a medium-term plan and timeline as regards phasing out the various tax exemptions. Stakeholder consultations should be an integral part of formulating this plan. An analysis of revenue forgone owing to the various tax exemptions should be provided in the next budget. This will draw much-needed political attention to this burning issue.

• In the FY23 budget, a new provision (Section 19F: Special Tax Treatment in respect of undisclosed offshore assets) was added to the Income Tax Ordinance 1984 to mainstream money earned and asset acquired abroad into the economy. According to the provision, no authority, including the income tax authority, shall raise any question as to the source of any asset located abroad if a taxpayer pays tax on such asset. This opportunity was to be in force for the full FY23 period. Such an initiative is ethically unacceptable, will discourage honest taxpayers, and has traditionally did not generate the intended revenue which justified its introduction in the first place. CPD strongly feels that this provision should be discontinued, and no such incentive finds its place in FY24 budget.

• Provisions such as Section 16H, Section 19BBBBB, and Section 19DD are still in place to legalise undisclosed income and assets under the Income Tax Ordinance, 1984. These should be discontinued from the next fiscal year.

• Since the income tax exemptions for 28 IT-enabled services (ITES) are set to come to an end in FY24, a thorough examination of the incentives should be undertaken with a view to (a) selection for continuation of incentives, (b) introduction of sunset clause and (c) identify opportunities for imposition of taxes on e-commerce and digital services. [The moratorium on e-commerce taxation, introduced in WTO in 1998, is set to come to an end by 2024 or 13th WTO Ministerial Conference – MC13, whichever is earlier if no agreement is reached in the WTO in this regard]. The government should take adequate preparation to (a) proactively participate in the WTO discussions and (b) identify tax measures if and when the moratorium comes to an end.

• Ambiguities in current tax laws (service code 99.60) in defining e-commerce activities should be removed to enhance the scope and opportunities of revenue mobilisation.

• To collect VAT at the local stage, NBR could install only 4,595 electronic fiscal devices (EFD) / sales data counter (SDC) machines at existing businesses against the target to reach the 10,000 mark by June 2022. Presenting the national budget for FY2023, the Finance Minister stated the plan to reach the target of installing 10,000 EFDs by June 2023. The government plans to install another 300,000 EFDs over the next five years, which is expected to yield an additional revenue of Tk 105.0 billion, with an initial 60,000 planned for FY24. NBR needs to aggressively pursue this target.

• NBR should launch at the earliest, a comprehensive online payment system for VAT, income tax and customs together with an interface with iBAS++ and ensure harmonisation and taxpayer data sharing across various wings of the NBR as has been envisaged in the PFM Action Plan 2018-23. The data-sharing issue has also been raised by the IMF.

• As per data from international sources, the larger part of Bangladesh’s illicit financial outflows are on account of trade mispricing. The Transfer Pricing Cell (TPC) of NBR, Bangladesh Financial Intelligence Unit (BFIU) and Customs Intelligence and Investigation Directorate (CIID) should work closely to deal with trade-based money laundering. For effective implementation of the responsibility of the TPC, the national budget for FY24 should ensure adequate allocation for technical and human resources and forensic investigation capacities of the aforesaid entities.

• The upcoming national budget must focus on generating revenue from specialised sources, particularly expediting the realisation of contested revenue claims through the Alternative Dispute Resolution (ADR) mechanism. [Regrettably, up to date data as regards this is not available on public domain. However, according to the NBR Annual Report 2019-2020, contested revenue claims in FY2020 amounted to more than Tk 1266.0 billion. ] Steps should be taken to expedite the resolution of pending tax-related cases in tax tribunals and courts.

• Priorities for public spending ought to be set out clearly in the FY2024 budget. The design of the budgetary framework should take cognisance of the rising cost of essentials. In order to do this, appropriate attention should be paid to food production, social safety net programmes (including public works programmes), subsidies for agriculture, energy and power sectors, as well as the health and education sectors. Supporting the marginalised groups should be the central focus of subsidy management.

• Prior government directives to reduce “unnecessary and luxury” public spending (such as the purchase of government vehicles and international travel) should be reintroduced.

• The ADP for FY24 should be carefully designed with a view to containing the budget deficit. A political government may find it tempting to take on new development initiatives in the run-up to the upcoming election by adopting a populist stance. The budget for FY24 should, however, refrain from any ostentatious public spending in the backdrop of the macroeconomic challenges facing the economy.

• The government should give priority to implementing all foreign-funded ADP projects in light of the current foreign exchange situation. The government should give higher priority to implementing projects that are nearly finished (about 90-95 per cent completion rate in June 2023).

• Projects that had a 10 per cent or lower implementation rate up till end-FY23 should be deprioritised. “Carryover projects” that have a maximum implementation rate of less than 30 per cent up till end-FY23 should be re-examined to justify continuation.

• The government should form an independent commission to assess the rising costs of public infrastructure projects. Concrete steps should be taken to ensure good governance in implementation of public infrastructure projects in particular. As a first step, the government must make all development project proformas (DPPs) available to the public for review and comments. To do this, the government should also think about undertaking a comprehensive assessment of public expenditures as early as possible.

Dr Fahmida Khatun is Executive Director, Centre for Policy Dialogue (CPD); Professor Mustafizur Rahman, Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem, Research Director, CPD; Towfiqul Islam Khan, Senior Research Fellow, CPD; Muntaseer Kamal, Research Fellow, CPD; Syed Yusuf Saadat, Research Fellow, CPD. towfiq@cpd.org.bd; avra.bhattacharjee@gmail.com

[Abu Saleh Md. Shamim Alam Shibly, Tamim Ahmed, and Helen Mashiyat Preoty, Research Associates of CPD; Lubaba Reza and Mohammad Abu Tayeb Taki, Programme Associates of CPD also contributed to the piece which is based on CPD’s Recommendations for the National Budget FY2023-24.]