Originally posted in The Financial Express on 3 January 2024

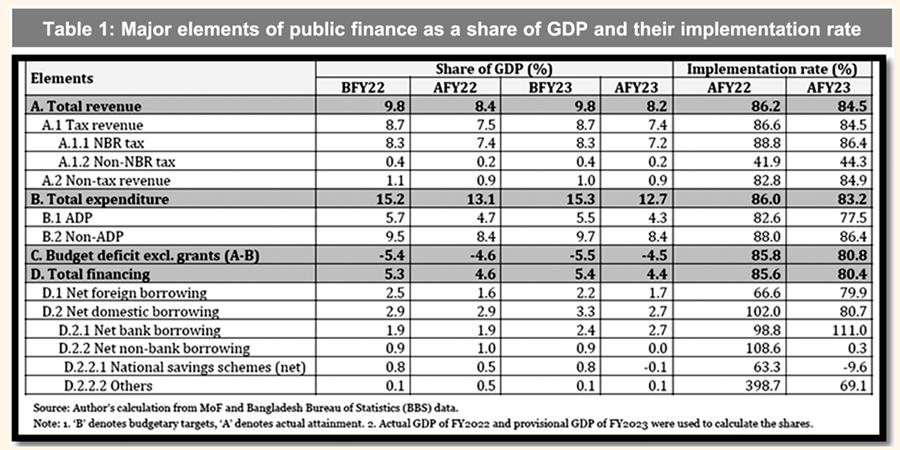

As a share of Gross Domestic Product (GDP), the country’s major public finance correlates were lower than the previous year. According to data from the Ministry of Finance (MoF), the revenue-GDP ratio of 8.2 per cent in FY2023 fell short of the budgetary target of 9.8 per cent. Regrettably, the revenue-GDP ratio in FY23 also declined when compared to the corresponding figure of FY22 (Table 1). Total public expenditure as a share of GDP also showed a similar trend. Within the components of public expenditure, annual development programme (ADP) expenditure as a share of GDP fell by 0.4 percentage points. The budget deficit (excluding grants) reached Tk. 1.98 trillion FY23 against the target of Tk 2.45 trillion. As a share of GDP, these figures were 4.5 per cent and 5.5 per cent, respectively (Table 1). A similar pattern was also observed in the case of FY22, where the budget deficit remained below its programmatic target.

Budget implementation slowed down. Total revenue collection recorded a 9.1 per cent growth in FY23 (2.0 per cent in FY22) against the target of 29.2 per cent. The majority of the attained growth in FY23 can be attributed to improved performances in income tax and value added tax (VAT) collection amid subdued import duty collection. Despite the higher growth in revenue mobilisation, total revenue shortfall (i.e., the gap between targeted and actual total revenue collection) has increased in FY23, reaching Tk 671.42 billion from Tk 537.91 billion in FY21. This implies that the implementation rate of revenue mobilisation decreased from 86.2 per cent in FY22 to 84.5 per cent in FY23 (Table 1).

The implementation rate of total public expenditure decreased to 83.2 per cent in FY23 from 86.0 per cent in FY22. Implementation rates for both ADP and non-ADP expenditure have slowed down. While the former declined to 77.5 per cent in FY23 from 82.6 per cent in FY22, the latter decreased to 86.4 per cent in FY23 from 88.0 per cent in FY22 (Table 1). In this connection, it needs to be noted that there is a discrepancy between the figures reported by the MoF and the Implementation Monitoring and Evaluation Division (IMED) of the Ministry of Planning (MoP). According to the IMED data, the ADP implementation rate in FY2023 was 78.2 per cent.

Some compositional shifts were observed within the domains of public finance. The share of NBR in total revenue declined in FY23 compared to FY22. Within public expenditure, the share of ADP expenditure fell to 33.8 per cent in FY23 from 35.9 per cent in FY22. The broad composition of budget deficit financing has remained largely the same in FY23. While foreign sources financed 39.2 per cent of the budget deficit in FY23 (36.0 per cent in FY22), 60.8 per cent was financed through domestic sources (64.0 per cent in FY22). However, within domestic sources, a significant shift was observed. While borrowing from the banking system constituted nearly two-thirds of the domestic borrowing in FY22, this share reached almost 100 per cent in FY23. Non-bank borrowing was utilised sparingly in FY23. Indeed, the government’s net borrowing from the issuance of national savings certificates, the major source of non-bank borrowing, was negative (Tk. [-] 33.47 billion) in FY23, as opposed to the budgetary target of Tk 350 billion.

Public finance situation in the early months of FY2024 and outlook: Timely availability of data has been a major impediment while assessing the public finance situation in FY2024, as MoF data is unavailable. As of December 2023, data from MoF, which provides the most comprehensive picture of the fiscal framework, is available only up to June 20233. While alternative sources (e.g., National Board of Revenue [NBR], IMED, Bangladesh Bank) provide public finance data in a more timely manner, it often comes at the cost of data accuracy and congruency (Bhattacharya et al., 2022). The analyses of the present section are constrained by these limitations.

According to the NBR data, tax collection by NBR increased by 14.4 per cent during the July-October period of FY24. This is a marginal increase from the corresponding figure for July-October FY2023, which stood at 14.2 per cent. The growth attained in the ongoing fiscal year was driven primarily by VAT and supplementary duty (SD) at the local level and income tax. The higher price level prevailing in the domestic economy is perhaps giving a push to the collection of VAT and SD at the local level. At the same time, import compression induced by government regulatory measures has resulted in an underwhelming performance of indirect taxes collected at the import level despite a considerable depreciation of the Bangladeshi Taka. Given the revenue-related conditionalities imposed by the International Monetary Fund (IMF), whether the pace of NBR’s tax collection is adequate remains a critical question.

As the IMED data shows, the implementation rate of the ADP was 17.2 per cent during the July-November period of FY24. This implementation rate was the lowest in the last five years owing to the sluggish utilisation of the ‘Taka’ component (i.e., the part of ADP that is financed by domestic resources). In this context, the crucial question is whether this resulted from the government’s cost-cutting efforts or the inability to carry out projects due to the foreign exchange crisis. On a positive note, within the components of ADP, project aid utilisation (19.2 per cent) was the highest in the last five years. This is particularly praiseworthy given the ongoing foreign currency situation.

Of the top ten ministries/divisions, constituting 70.2 per cent of the ADP allocation for FY24, six were unable to utilise their respective allocations at the average level. These include the Road Transport and Highways Division, Secondary and Higher Education Division, Ministry of Science and Technology, Health Services Division, Ministry of Primary and Mass Education, and Ministry of Water Transport.

As per Bangladesh Bank data, budget deficit financing during the July-October FY24 period was overwhelmingly dependent on non-bank borrowing. Non-bank borrowing increased substantially from Tk. 27.49 billion during July-October FY23 to Tk 121.67 billion during July-October FY2024. The net sale of national savings certificates (NSCs) was negative to the tune of Tk. (-) 23.05 billion during the July-October period of FY24. Net foreign financing decreased by 24.8 per cent to Tk 105.66 billion during the period under review.

The outlook for the rest of the months suggests that the revenue collection target for FY23 is unlikely to be met. The IMF has already slashed the target for tax collection for FY2024 by more than Tk 550 billion while setting the corresponding indicative target compared to the programmed national budget target. Consequently, public expenditure will need to be restrained to keep the budget deficit in check. More importantly, non-bank borrowing is likely to be well below target as NSD sales may continue to be sub-par owing to lower savings with people and creeping interest rates for deposits with banks. Hence, bank borrowing will be under pressure to service the budget deficit. In view of the liquidity pressure with the commercial banks and the government’s commitment not to opt for borrowing from the central bank, the fiscal space available for the government is somewhat limited. Hence, the government may need to continue a restrained fiscal approach to maintain discipline in the macroeconomic management.

As part of the IMF conditionalities, Bangladesh has to meet several performance criteria (PC), indicative targets (ITs), structural benchmarks (SBs), and reform measures (RMs) in a timebound manner. Besides these, a number of related policy recommendations were suggested by the IMF. At the end of FY23 (i.e., June 2023), Bangladesh was able to meet the PC on primary balance as public expenditure slowed down. The continuous PC regarding external payments arrears was also met. While the IT on tax revenue mobilisation was missed, the targets on priority social spending and capital spending for the end of June 2023 period were attained. The SB of MoF adopting tax revenue measures yielding an additional 0.5 per cent of GDP in the FY24 budget was also met.

Bangladesh will need to meet a number of PC, ITs, and SBs alongside implementing several policy recommendations during FY24.

Among the conditionalities set by the IMF concerning public finance, the majority of the SBs are related to strategy/plan documents and policy notes, which are ‘relatively easy to meet’. Regrettably, the IMF document does not adequately specify the quality assurance aspects of these documents. The plan to reduce dependence on NSCs also goes along well with the present dynamics. The IT regarding tax revenue mobilisation is likely to be missed by the end of FY24 and might have a negative impact on maintaining the PC on the primary balance unless the public expenditure is adequately downsized. Hence, missing the target related to tax collection might adversely affect the ITs on priority social spending and capital investment, as emphasising such public expenditure would require incremental revenue. Some of the conditionalities will require further detailing regarding their methodology (e.g., price adjustment mechanism for petroleum products) and stakeholder engagement plan in the coming days. Regrettably, the IMF conditionalities do not mention anything regarding ensuring value for money for public investment as part of the programme.

Recommendations for the upcoming medium and long term revenue strategy: The revenue-GDP ratio is arguably the most disappointing indicator in the context of Bangladesh’s development trajectory. The key challenges in this context are the inability to implement the planned reforms in a timely manner, establish good governance and improve tax administration. To secure the IMF loan, the government has recently implemented some of the long-overdue reforms, sometimes without adequate stakeholder discussions. A medium and long term revenue strategy (MLTRS) is currently being developed that is expected to chart a pathway to enhance revenue collection over the next five years or so. The strategy is expected to be adopted by June 2024. The strategy will be a successor to many such past strategies, including the previous NBR modernisation plan, Customs Modernization Strategic Action Plan 2019-2022, VAT Improvement Program (VIP) 2015-2021 and ongoing Public Finance Management (PFM) Reform Action 2024-2028. The strategy should take the following recommendations into cognisance.

First, it is critical that the strategy prioritises the unfinished agenda, including the actions required to operationalise the aforesaid reforms (e.g., installing electronic fiscal devices, enhancing the number of registered taxpayers and promoting digital methods such as e-TDS, ereturn, e-BIN, iVAS, VAT Calculator, e-payment, A-Challan etc.). The stakeholders’ concerns regarding the latest reforms, including the Income Tax Act 2023 and the Customs Act 2023, should be discussed for further professional scrutiny involving multi-stakeholders. Similarly, revisiting the prevailing tax exemptions through detailed data analysis should be high on the agenda with a view to ensuring policy predictability.

Second, the strategy needs to recognise the frontier issues of taxation in the context of Bangladesh, such as meaningfully taxing property and wealth and the expanding digital economy. CPD has recently undertaken two studies in these areas. Recommendations put forward in these studies can benefit the formulation of the MLTRS.

Third, improving the data ecosystem should be at the heart of the new strategy. It is to be noted that data constraints put challenges in addressing tax evasion and estimating tax expenditure and exemptions. Hence, the issue of interoperability of data, not only within an agency such as NBRbut also across regulatory agencies, should be taken into cognisance. The strategy concerning revenue data should be linked with other aspects of PFM, including public expenditure and debt management.

Fourth, the strategy should uphold the curbing illicit financial flow (IFF) agenda. IFF has often been undermined by the tax authorities at the operational level. The National Strategy for Preventing Money Laundering and Combating Financing of Terrorism was last formulated for the period of 2019-2021, with the Bangladesh Financial Intelligence Unit (BFIU) being the coordinating agency, which identified 11 strategies and 137 action items involving dozens of regulatory agencies. The first strategy identified was regarding addressing IFF, where NBR was recognised as a key agency. It needs to recognise that many of the actions planned under the strategy were not fully implemented. The MLTRS must revitalise and upgrade these actions, taking an appropriate multi-agency approach.

Fifth, the digitalisation of the entire revenue system should lead the strategy. The issue of digitalisation has been recognised as a priority reform agenda for some time now.6 Regrettably, the progress remained less than satisfactory. Technological upgradation of tax administration is critical to this end. The digitalisation process should also be sustainable, considering the required flexibility and putting adequate resources – both financial and human resources.

Sixth, the scope of the MLTRS should be properly defined. Apparently, NBR is in the driving seat in developing the strategy. However, a comprehensive revenue strategy should recognise the role of other sources and agencies beyond NBR’s remit. This includes government agencies, stateowned enterprises and local government entities.

Seventh, two sets of evidence and learnings should inform the MLTRS formulation process. While revenue mobilisation is the primary objective of the strategy, the economy-wide implications and equity concerns should not be undermined. Also, an assessment of past reform initiatives that identifies the reasons behind lacklustre progress and learnings for the present strategies should accompany the MLTRS.

Finally, the entire strategy development process should be carried out with openness and transparency. The concerns of all stakeholders should be taken into consideration and addressed. It may be assumed that the strategy will trace out a time-bound action plan where the roles of the involved agencies are well identified, and the monitoring mechanism and accountability process should also be clearly stated. The adoption of this strategy will indeed require political buy-in not only from high-level policymaking but also from the operational level. Besides developing MLRTS, the government should review public expenditure, particularly considering the high cost of public investment projects and formulate a strategy to ensure value for public money.

Dr Fahmida Khatun, Executive Director, Centre of Policy Dialogue (CPD); Professor Mustafizur Rahman, Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem, Research Director, CPD; Mr Towfiqul Islam Khan, Senior Research Fellow, CPD; Mr Muntaseer Kamal, Research Fellow, CPD; and Mr Syed Yusuf Saadat, Research Fellow, CPD. towfiq@cpd.org.bd ; muntaseer@cpd.org.bd.

[Research support is given by Mr Tamim Ahmed, Senior Research Associate; Ms Marium Binte Islam, Research Associate; Mr Mahrab Al Rahman, Programme Associate; Ms Anika Ferdous Richi, Programme Associate; Ms Zazeeba Waziha Saleh, Programme Associate; Mr Rushabun Nazrul Yaanamu, Research Intern; and Mr M M Fardeen Kabir, Surveyor, CPD.]